Corona casts shadow over export earning,Platform of Bangladesh’s garments exporters, BGMEA, confirmed that $2.87 billion worth of export order cancelled before March 30. Evidently, Coronavirus outbreak unleashes its harming effect on economy. Unarguably, this pandemic may affect more or less all the forex earning sources. Less pledges of foreign assistance are made for the ongoing fiscal year. There is little room for optimism for coming fiscal year. As it appears, our Debt Service Payments may also take a hit because of pandemic crisis.

It starts alarm bell ringing

Over debt service payment.

Disaster means weak debt management,

Reflected in lower annual installment.

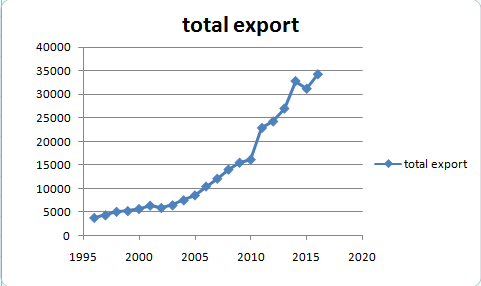

I did a little analysis on debt service payments and total export based on 20-year-long data from 1996 to 2016. Debt Service Payments largely depend on forex earnings. Export is one of the key sources of forex earnings. What kind of influence export has on debt service was what I would like to see. Data gleaned from Bangladesh Economic Review.

As usual, I first went for autocorrelation check. Durbin-Watson statistic was found to be 1.46 for 21 observations and 1 explanatory variable. So there was no autocorrelation. It reported positive autocorrelation

(Source:Bangladesh Economic Review 2018)

🔺 Debtt = a + b Debtt-1 + ct

🔺 Exportt = a + b Exportt-1 + ct

Where 🔺 Debtt= Differences in debt services at t,

Debtt-1 = Debt service payments at t-1,

🔺 Export t= Differences in export earnings at t,

Exportt-1= export earnings at t-1,

t = a time trend variable, here year.

To my dismay first differences of Debt and Export did not turn out to be stationary. So both Debt and Export, for the sake of simplicity, were integrated of order d, I(d).

Regressing Debt on Export I got the residuals for cointegration test. Then I ran the following regression:

🔺 Residt = b Residt-1 + c 🔺 Residt-1

The computed tau statistic of lagged residual's slope coefficient, -3.94, was greater than Engle-Granger critical statistic at 5% level in absolute terms, -1.94. So I rejected the null hypothesis of no cointegration or residuals are nonstationary. There was indeed a cointegrating relationship between the two and residuals appeared to be stationary.

This kind of situation, variable were I(d) series and cointegrated, requires a VEC model :

🔺 Debtt = p + q Residt-1+ vtDebt

🔺 Exportt = r + s Residt-1+ vtExport

where Residt-1= lagged residuals obtained from regressing Debt on Export Resulting model looked like this:

🔺 Debtt = 33.083 -0.508 Residt-1(F=2.19, p=0.155)

(t=1.84, p=0.08) (t=-1.48, p=0.155)

🔺 Exportt = 1483.07 + 4.47 Residt-1(F=0.276, p=0.605)

(t=3.334, p=0.033) (t=.525, p=0.605)/>

None of the individual functions and slope coefficients appeared to be significant. However I was eager to see impact of a shock to Export on Debt Service Payments. As usual I depended on Impulse Response Function(IRF), which shows the effect of a shock to an endogenous variable on itself and on other endogenous variables.

Later I turned to see whether disaster years, be it natural or political or international, had any effect on debt service payments. I constructed the following regression function:

lnDebtt = a1 + b Export t+ a2Dt

where lnDebtt = log natural of debt service payments at t,

Export t = export earnings at t

D = 1 for disaster years,

= 0 for normal years.

This model turned out to be significant (F= 90.15, p = 0.00, degree of freedom = 2, 18) Resulting resulting regression function looked like this:

lnDebtt = 6.20 + 0.000028 Export t- 0.0657Dt

The dummy coefficient , however, appeared to be insignificant (t = - 1.50, p = 0.15). Had it been significant, it would be said that debt service payments in disaster years were 6.36% lower than those in normal or calm years.

More or less it is becoming clear that Coronavirus may affect our debt service payments by harming our forex earning sources. Any drop in debt service payments in disaster years may put pressure on subsequent years. As external assistance pledges are not on the surface, government may go for costly options for foreign borrowing coupled with significant scrapping of development projects at home.

No comments:

Post a Comment